Estimating your car insurance cost without speaking to an agent is possible when you know which factors insurers evaluate and which tools simplify the process. Online calculators, insurer websites, and expert guidelines help you project premiums with reasonable accuracy.

What Determines Car Insurance Costs?

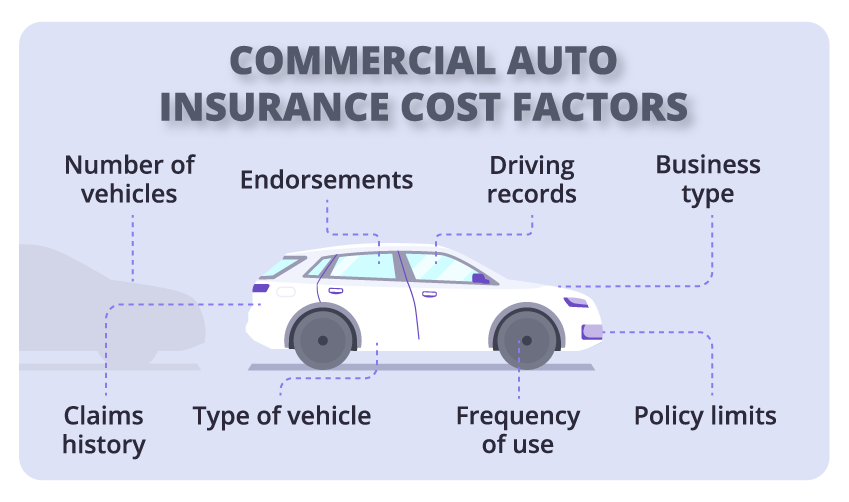

Car insurance costs depend on measurable risk factors. Insurers use rating models that analyze your profile and driving behavior.

Key factors include:

-

Driving history: Accidents, speeding tickets, or claims increase rates.

-

Vehicle type: Sports cars or luxury vehicles cost more to insure than sedans.

-

Location: Urban ZIP codes often carry higher premiums than rural areas.

-

Coverage limits: Comprehensive and collision raise costs compared to liability-only.

-

Credit score (in most states): Lower scores correlate with higher rates.

-

Annual mileage: More miles increase exposure to risk.

-

Age and experience: Young or inexperienced drivers face higher premiums.

Insurers weigh these attributes differently, but each one contributes to your estimated price.

How Can You Estimate Car Insurance Online?

You can estimate your premium without an agent by entering your details into a digital tool. Online calculators approximate what major insurers would charge by applying their underwriting models.

Try the car insurance calculator to receive a quick estimate.

Which Tools Help You Calculate Insurance Costs?

Different resources allow you to estimate costs before committing to a policy:

-

Car insurance calculators – Enter vehicle details, driving history, and coverage needs for an instant estimate.

-

Insurer websites – Major carriers provide quote forms that display projected monthly or annual rates.

-

Comparison platforms – These aggregate multiple quotes based on your single entry.

-

State insurance department guides – Some states publish average premium charts by age, ZIP code, and vehicle type.

Each option helps you anticipate expenses without calling an agent.

What Does Expert Advice Say About Estimating Insurance Costs?

Lori Wray, AAI, a licensed insurance advisor at Matrix Insurance, emphasizes that calculators are reliable for estimates but not substitutes for personalized guidance. According to Wray, calculators help drivers understand coverage-price relationships, but final premiums depend on underwriting reviews.

Her advice: “Use calculators to set expectations, then review coverage with a licensed advisor to confirm protection aligns with your needs.”

What Information Should You Gather Before Estimating?

To get accurate numbers, you need specific information ready:

-

Vehicle Identification Number (VIN)

-

Year, make, and model of the car

-

Current odometer reading

-

Average miles driven per year

-

Driving record details (accidents, tickets, claims)

-

Desired coverage type and limits

-

Address where the vehicle is garaged

Providing complete and accurate data improves the reliability of online estimates.

How Do Coverage Choices Change Premiums?

Coverage levels directly affect your estimate.

| Coverage Type | Impact on Cost | Example Monthly Difference* |

|---|---|---|

| Liability only | Lowest | $60 – $90 |

| Liability + collision | Moderate | $120 – $160 |

| Full coverage (incl. comprehensive) | Highest | $170 – $240 |

*Estimates vary by state and driver profile.

Adding roadside assistance, rental reimbursement, or higher liability limits raises premiums further.

Why Should You Re-Estimate Annually?

Car insurance premiums shift over time. Annual re-estimation helps you identify cost changes caused by:

-

Policy renewals with adjusted rates

-

Life events (moving, marriage, job changes)

-

Vehicle upgrades or aging

-

Improved driving history or credit score

Monitoring these changes ensures your coverage remains cost-efficient.

What Is the Next Step After Estimating?

After estimating your premium online:

-

Compare rates from at least three insurers.

-

Adjust deductibles and coverage limits to balance protection and affordability.

-

Consult a licensed professional, such as Lori Wray, AAI, to verify accuracy and receive tailored advice.